Visualisations

Diagnostic Charts

Publication-quality plots generated from the full BTC-USD dataset.

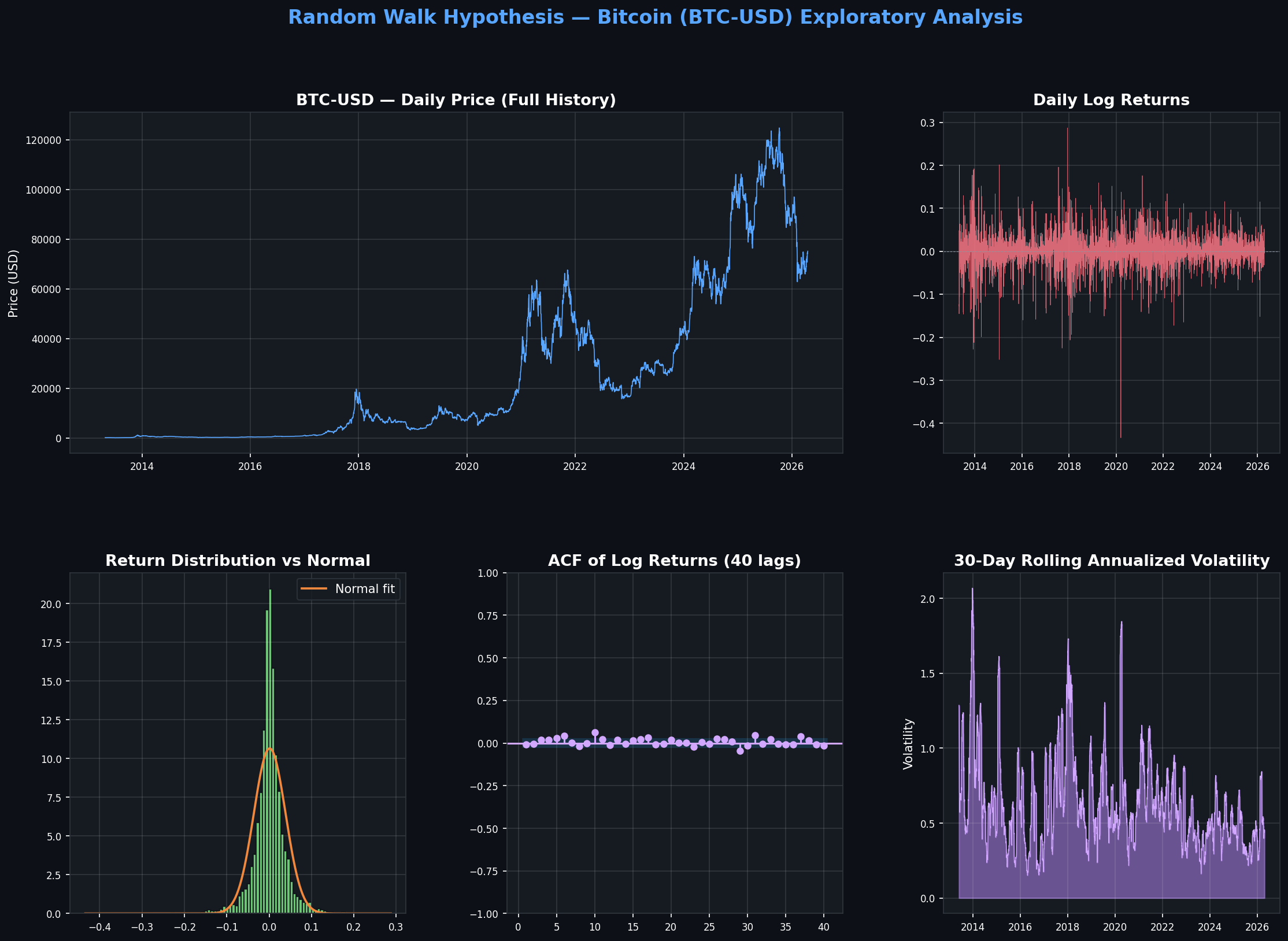

Exploratory Data Analysis

Price series, log returns, return histogram, ACF, and 30-day rolling volatility.

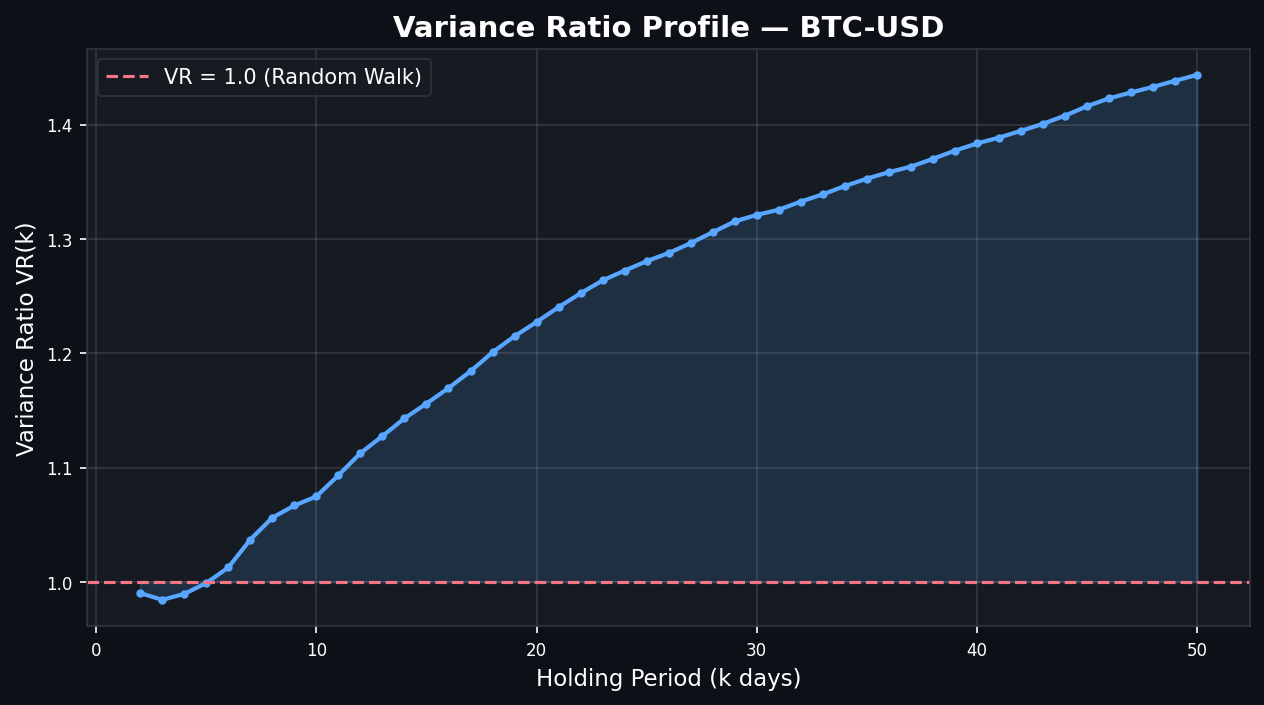

Variance Ratio Profile

VR(k) from k=2 to k=50. Monotonically rising curve confirms long-run momentum.

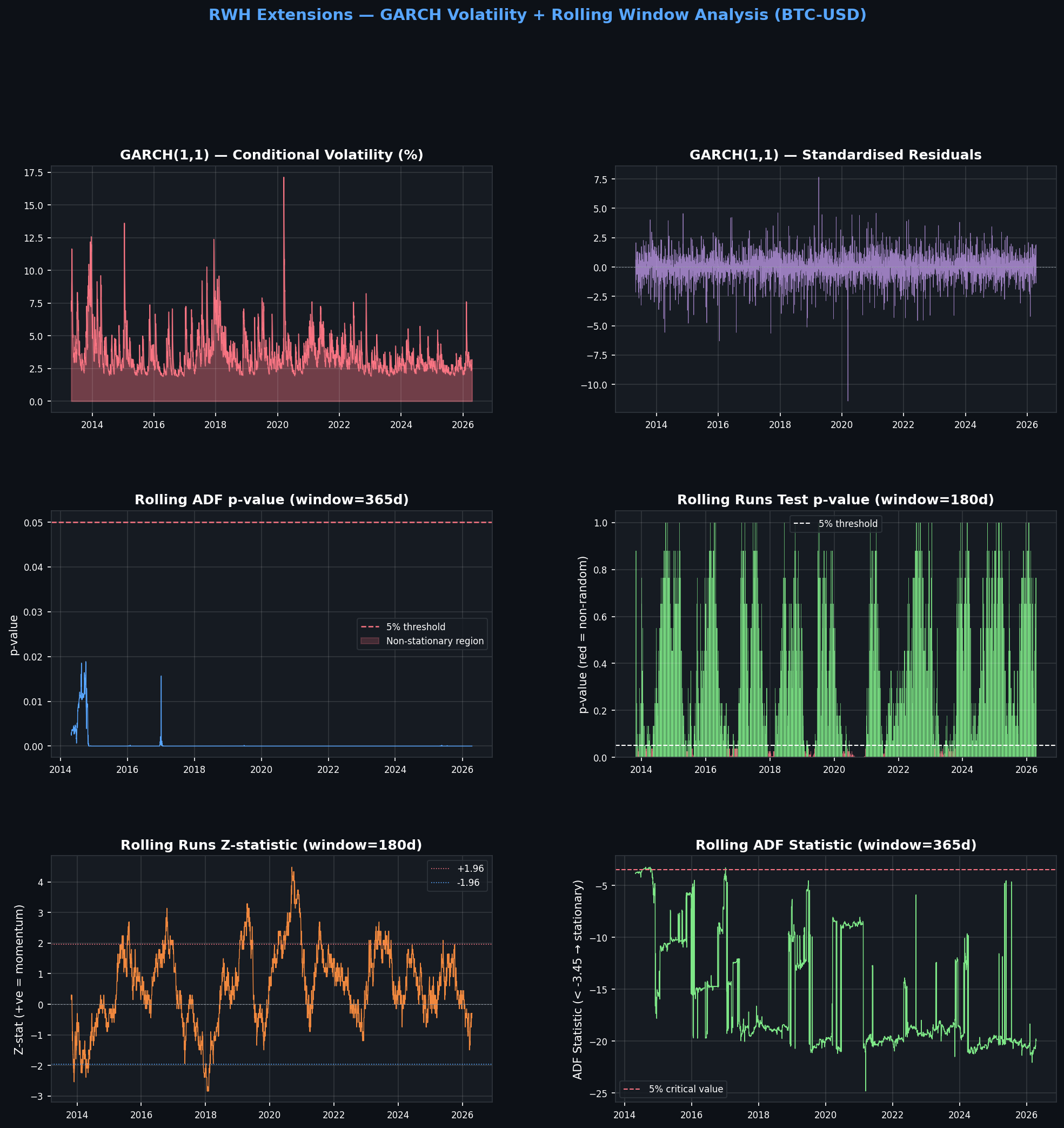

GARCH + Rolling Window Analysis

Conditional volatility, standardised residuals, rolling ADF and Runs statistics.